It’s a new approach to designing trading strategies and it’s pretty exciting.

But first, let me give you some overview.

As many of you already know, I’m currently running two investment programs in my hedge fund. One is based mainly on daytrading breakout strategies, and the second one on swing breakout strategies. (Both of them have a very low mutual correlation, as I shared in this post).

Now, our goal is to launch another, 3rd investment program. And of course, the goal is to get as low correlation to the existing two programs, as possible.

So, I started brainstorming with my hedge fund team how we can achieve that. And we decided to take several experimental steps, to come up with a fresh, new generation of trading strategies.

One of the steps is to use Market Internals as an entry method.

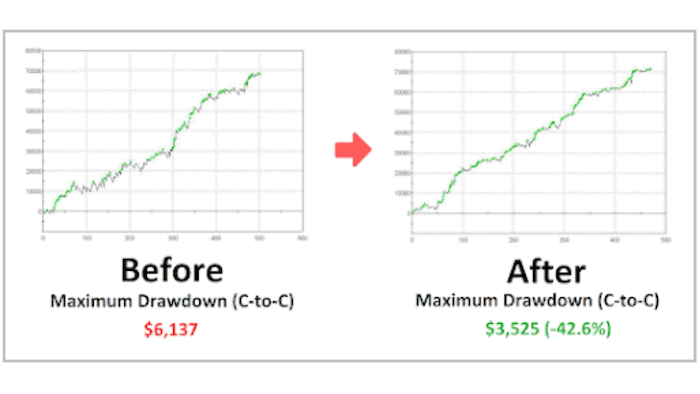

Market Internals is the “secret weapon” I originally developed to lower drawdowns. And it’s what Max Schulz used to claim 3rd place in the World Cup Trading championships in 2017.

My original application uses Market Internals as an additional “super-filter” to existing trading strategies. So “the bigger market picture” can be taken into consideration. And drawdowns lowered drastically as a result.

Want MORE? Sign up for the free BTA newsletter and join 1000’s of other traders who receive meaningful trading content every week, straight into your email inbox. Click here to join us.

But this time, I asked myself:

How about I use these Market Internals “super-filters” as standalone entry conditions?

So, the last few days I spent taking all the Market Internals conditions that I share in the ‘Trading Market Internals’ program and using them as entry conditions.

I basically took each of the conditions, one after another, added a simple stop-loss and profit-target, and watched what happens. To see if the idea is even viable. (Please, bear in mind: I’m talking about a strategy DESIGN stage in this article, not about final strategies yet).

And to my pleasant surprise, some of the Market Internals conditions, used as entries, showed to be more than viable.

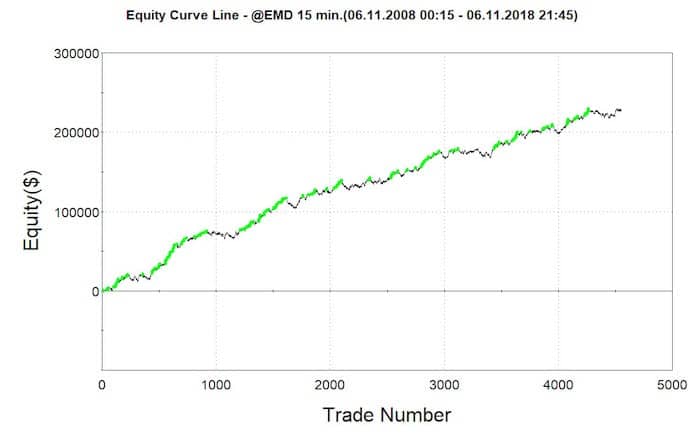

With the best conditions, I got strategy prototypes like this:

Now, of course, this is still a PROTOTYPING phase only. So no robustness tests yet. No transaction costs yet. But also NO FILTERS yet. This is the roughest, simplest way of using my Market Internals conditions as entries. Yet, even without any additional filters, the first prototypes are more than promising.

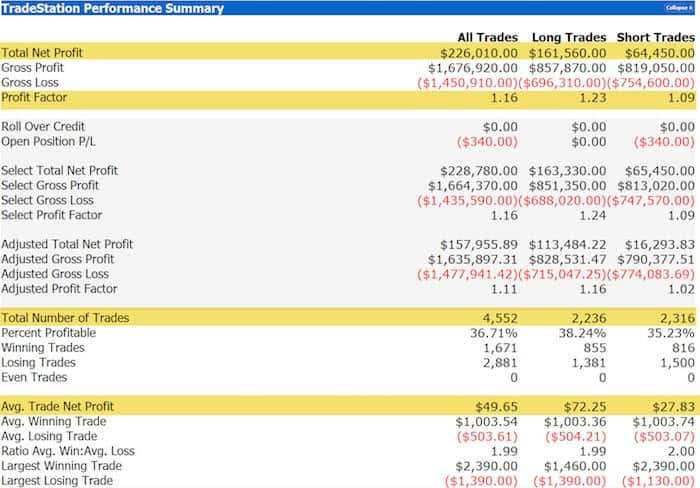

Let’s take a look at where I see the strong and weak sides looking at the performance report:

First of all, the sample size (Total Number Of Trades) is HUGE. I have never experienced such a huge sample size on a 15-minute chart. 4,552 trades are giving me very high statistical significance, which is always a good thing to have.

Now, the Net Profit, for just a single strategy, is also HUGE. I have never seen 226,000 USD Net Profit in 10 years with my breakout strategies on a 15-minutes chart neither. That is about 22,000 USD per year on average. And that is pretty outstanding.

Where I see weakness, is the short side of this prototype.

The Average Short Trade is almost ⅓ of the long side. With 27.83 USD, it is far from being satisfactory. Transactional costs will destroy all the short trading. Plus the Profit Factor 1.09 on the short side is very low too.

But again, this all is before any filters.

I’m pretty sure that once I start testing the filters I normally use for my breakout trading strategies, things will get much better. Which, of course, is another step.

But for now, here are my first conclusions and also the reason I shared my current work with you:

| 1. | The know-how I share in the ‘Trading Market Internals’ program can definitely be used far beyond reducing drawdowns. From my recent preliminary testing and prototyping, I can already confidently say that Market Internals can perfectly serve as powerful, fresh trading entries too. |

| 2. | My massive robustness testing procedures (the same I use for my breakout trading strategies), need to be applied. But after I add some of my proven long-term filters, I’m more than confident that at least some of the prototyped candidates will pass. The majority will not (as usual), but some of them very likely will. The reasons I’m staying highly optimistic are:

a) With the amount and diversity of my Market Internals conditions and the proven, robust filters, there will be a rather high number of prototypes. And that means dramatically increased chances that at least some will pass. b) The preliminary testing and prototyping brought highly satisfactory results already. My experience with similar previous preliminary prototyping and testing suggests that there is a true edge in some of the prototypes. |

| 3. | Just by looking at the Market Internals entries on a chart, and comparing them with my regular breakout entries, the low correlation I desire shouldn’t be a problem to achieve. But of course, only if some of the prototypes pass the robustness testing procedures. So, let’s hope that luck will be on our side and my current work is going to serve as a good foundation for our 3rd investment program. |

Again and again, I am blown away by the power and versatility of Market Internals. How much they can do for you, for your trading. Definitely one of the best tool I have discovered – EVER.

If you still are not familiar with Market Internals, download the FREE report with 3 case studies.

Happy trading!

Tomas

![[VIDEO] Beat the markets with better ideas](https://bettertraderacademy.com/wp-content/uploads/2018/06/Beat-the-markets-with-better-ideas2-1-min.png)

![[VIDEO] How traders get high (without weed)](https://bettertraderacademy.com/wp-content/uploads/2019/07/8jul19-v2-min.png)